The Complete Risk & Reward Guide

If you’re looking for waterfront homes Connecticut right now, you already feel the pull. These properties offer something most homes never can: your own piece of the water, morning coffee on the dock, and views that change with every season.

As of February 2026, waterfront inventory across Connecticut is extremely tight — only about 351 active listings statewide. New shoreline listings dropped another 6% last month while prices in coastal towns rose 12.6% year-over-year. Buyers from New York City, Boston, and retirees are moving fast.

vrbo.com Luxury Waterfront Home Sleeps 16 Game Room Private Beach and Dock – Mason’s Island | Vrbo

Private dock and luxury waterfront home on a Connecticut shoreline — the kind of lifestyle buyers are chasing in 2026.

The rewards are powerful: private waterfront access, strong appreciation that often beats inland homes, prestige, and a lifestyle you can’t replicate anywhere else.

Aerial view of prime Long Island Sound waterfront real estate in Connecticut.

But 2026 also brings real risks that catch many buyers off guard — updated flood zones, rising insurance costs, stricter shoreline rules, and structural issues that only show up after a big storm.

I’m Steve Schappert, your customer-first Connecticut real estate broker with 45 years of hands-on experience. I’ve helped hundreds of families buy waterfront homes, renovated over 1,300 properties, and built 12 homes — including waterfront projects where I’ve seen exactly what works and what becomes a costly surprise.

Most brokers just show the pretty pictures. I bring real construction knowledge so you understand the true risks and rewards before you ever write an offer.

This complete 2026 guide walks you through everything: current flood zones, insurance changes, shoreline regulations, structural red flags, pricing trends by lake and river, real buyer case studies, and a step-by-step checklist to buy safely.

Whether you’re dreaming of Long Island Sound frontage, a quiet cove on the Connecticut River, or a peaceful lot on Candlewood Lake, this guide will help you make the smartest decision possible.

Let’s separate the dream from the details — so your waterfront purchase in Connecticut becomes one you’ll love for decades.

The Rewards of Owning Waterfront Homes in Connecticut in 2026

Sunset from your own dock — one of the daily rewards of waterfront living in Connecticut.

The rewards of owning waterfront homes Connecticut in 2026 are stronger than ever.

Inventory remains extremely tight, with only a few hundred true waterfront listings across the entire state. At the same time, demand from New York and Boston buyers plus retirees continues to climb. The result is steady price growth that has outpaced most inland neighborhoods for the past several years.

Here’s what buyers who act now are actually getting:

- Your own private waterfront lifestyle Step outside your door to a dock, private beach rights, or direct river access. Kayak before breakfast. Watch the sunset from your deck instead of a screen. Swim, boat, or simply enjoy the water views every single day.

Kayaks ready on the lawn — summer fun at a Connecticut lakefront home.

- Stronger long-term appreciation Waterfront and shoreline properties in Connecticut have consistently delivered higher returns than standard suburban homes. In early 2026, premium waterfront segments are seeing year-over-year gains well above the statewide average, driven by limited supply and lifestyle demand.

- Prestige and generational wealth A waterfront address carries real status in Connecticut. These homes also tend to hold value exceptionally well and appeal to the widest pool of future buyers — from young families to empty-nesters to international buyers looking for a Northeast waterfront retreat.

- Four-season enjoyment Summer boating and swimming, fall foliage on the water, winter walks along a frozen lake or river, and spring wildlife returning to the shoreline. Connecticut waterfront gives you true year-round living that most properties simply can’t match.

As your Connecticut real estate broker, I’ve helped hundreds of families make this move over the past 45 years. The comment I hear most often a few years after closing is simple: “We should have done this sooner.”

These rewards are very real — and very achievable in 2026.

But here’s the part most buyers miss: the rewards only stay rewarding when you fully understand the risks that come with waterfront ownership. In the next section we’ll look at the most important one — flood zones — and exactly how to evaluate them before you fall in love with a property.

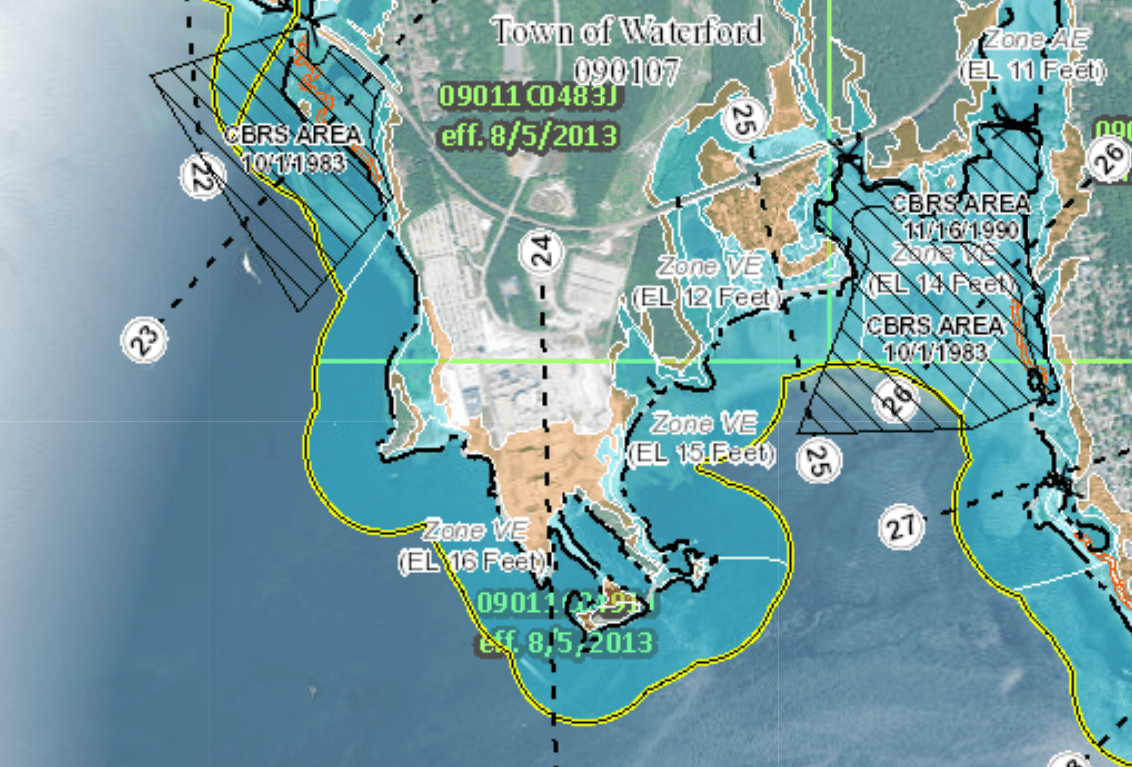

Flood Zones in Connecticut: How to Know Your True Risk Level

FEMA flood zone map showing high-risk areas along the Connecticut coast — every waterfront buyer needs to understand this.

Even the most beautiful waterfront homes Connecticut can come with hidden flood risks that affect everything from insurance costs to resale value.

FEMA divides properties into flood zones. Here’s what every buyer needs to know in simple terms:

- Zone VE – Highest risk coastal areas with waves 3 feet or higher during a 100-year storm. These properties almost always require flood insurance and elevation.

- Zone AE – Areas with a 1% annual chance of flooding (base flood elevation shown on maps). Still high risk, but usually less wave action than VE.

- Zone X – Moderate or low risk (500-year flood or minimal flooding). Many buyers assume “Zone X means safe,” but that’s not always true near the water.

In 2026, new FEMA map updates are hitting Fairfield, New Haven, and parts of New London counties especially hard. Some properties that were Zone X just a few years ago are now being reclassified into AE or VE.

Close-up of a FEMA flood zone map for a Connecticut shoreline town — notice the VE and AE zones right along the water.

As your Connecticut real estate broker with 45 years of construction experience, I always tell clients: never trust the listing agent’s flood zone claim alone. I order a professional flood determination report and elevation certificate on every waterfront property before we make an offer.

Here’s what I look for:

- Exact Base Flood Elevation (BFE) on the map

- How high the finished floor sits above that elevation

- Whether the home is in a Coastal High Hazard Area (V zone)

- Any recent map changes that could raise insurance costs dramatically

One quick story: I had a client fall in love with a gorgeous home on the Connecticut River. The listing said “flood zone X.” When we pulled the real data, it was actually AE with a low elevation. We walked away and found them a better property that saved them thousands in insurance and future headaches.

Knowing your true flood risk level early is the single smartest step you can take when buying waterfront real estate Connecticut in 2026.

Once you understand the flood zone, the next big question is money — how much will flood insurance actually cost you? That’s what we cover in the next section.

Flood Insurance Changes Coming in 2026 – The Numbers That Matter

Storm waves crashing against waterfront homes in New Haven, Connecticut — this is exactly why flood insurance has become one of the biggest costs (and surprises) for buyers in 2026.

Flood insurance is no longer optional on most waterfront homes Connecticut — and the rules changed dramatically under FEMA’s Risk Rating 2.0 program.

Here’s what every buyer needs to know right now:

- NFIP premiums are rising sharply Many waterfront policies saw 15–18% increases in 2025, and the same annual hikes are built in for 2026. Some properties that were $2,800 a year two years ago are now $5,500–$8,000+.

- New FEMA maps = new classifications As maps get updated in 2026, properties that used to be moderate risk (Zone X) are moving into AE or VE zones. That single change can double or triple your annual premium overnight.

- Mandatory disclosure law takes effect in 2026 Sellers must now provide the current flood insurance cost and flood zone in writing before contracts are signed. No more surprises at closing.

This waterfront home in Westbrook, Connecticut was lifted on pilings to reduce flood risk and lower insurance costs — a smart move more buyers are making in 2026.

As a Connecticut real estate broker who has renovated over 1,300 homes and built new ones, I always run the numbers early. I’ve seen clients save $3,000–$6,000 a year by choosing an elevated home or adding flood vents and breakaway walls.

Private flood insurance is now often cheaper than NFIP for many waterfront properties, but it comes with different coverage limits and deductibles. I help my clients compare both options side-by-side so they choose the right policy for their budget and risk level.

Real-world 2026 examples I’m seeing right now:

- Moderate-risk lakefront on Candlewood: $2,100–$3,400 per year

- Direct Long Island Sound frontage in Zone AE: $6,800–$11,500 per year

- High-velocity VE zone property: $12,000–$18,000+ per year (some buyers walk away when they see this)

Bottom line: flood insurance is now one of the largest ongoing costs of owning waterfront real estate Connecticut. Ignoring it or assuming “it won’t be that bad” is the fastest way to turn a dream home into a financial burden.

In the next section we’ll look at shoreline regulations and permits — another area where many buyers get caught off guard.

Shoreline Regulations & Permits Every Buyer Must Understand

Stone seawall and private dock on a prime Connecticut waterfront property — beautiful, but every change requires permits.

Connecticut’s shoreline is one of the most tightly regulated areas in the Northeast, and many buyers discover this too late.

The state’s CT DEEP Coastal Management Program and the public trust doctrine control almost everything that touches the water. Here’s what matters most for waterfront homes Connecticut buyers in 2026:

- Mean High Water Line Anything below this line is generally public property. You can’t just extend your yard or build a new seawall without state approval.

- Docks, piers, and boat lifts Even repairing an existing dock usually needs a permit. New docks or expansions can take 6–18 months and often require neighbor notifications and environmental reviews.

- Seawalls and bulkheads Repairing or replacing a failing seawall is heavily scrutinized. You must prove it’s necessary and use approved materials and designs.

Installing a new steel bulkhead along the Connecticut shoreline — a major permitted project that can cost $150,000–$400,000+.

As your Connecticut real estate broker with 45 years of hands-on construction experience, I’ve walked through these processes many times. I know which towns are strict (Greenwich, Darien, Westport) and which are a little more straightforward (parts of the Connecticut River or Candlewood Lake).

Pro tip from real deals I’ve closed: Always get a marine contractor and a land-use attorney involved before you make an offer. A $25,000 pre-offer consultation can save you $200,000 in headaches later.

If you’re thinking about building new or doing major work on waterfront real estate Connecticut, these regulations can limit what you’re allowed to do — or add significant time and cost to your project.

Now that you understand the rules around the water’s edge, the next critical piece is what’s happening underneath and around the house itself — the structural red flags that only someone with real building experience spots right away.

Structural Red Flags: What 45 Years of Construction Experience Has Taught Me

Active shoreline erosion eating away at a Connecticut waterfront property — one of the most common (and expensive) problems I see.

After 45 years renovating over 1,300 homes and building 12 new ones — many on the water — I’ve learned that the prettiest waterfront homes Connecticut can hide the costliest problems.

Here are the structural red flags I personally check on every waterfront showing:

- Shoreline erosion and failing seawalls Waves and ice slowly undermine the land. A seawall that looks fine today can fail in the next big storm. Repair or replacement often runs $150,000–$500,000+ depending on length and materials.

Foundation crack caused by water pressure and settling — a classic issue on older waterfront homes.

- Foundation and elevation problems Many older waterfront homes sit too low. Water infiltration causes cracks, bowing walls, and mold. I’ve seen homes where the entire first floor had to be lifted — a $100,000–$300,000 job.

- Septic systems and wells too close to the water High water tables and flooding can contaminate wells or cause septic failure. Replacing a failed septic near the shoreline easily costs $40,000–$80,000 and requires special permits.

- Storm surge and wave vulnerabilities Older homes without proper breakaway walls, flood vents, or elevated utilities get destroyed in major storms. I’ve walked through properties after Irene and Sandy where the damage was entirely preventable.

As your Connecticut real estate broker who actually understands construction, I don’t just point these out — I help you price them in or walk away. I’ve saved clients hundreds of thousands by spotting issues early and negotiating repairs or credits before closing.

The biggest mistake I see? Falling in love with the view and ignoring what’s happening under and around the house.

Once you know these red flags, the next step is understanding what you’ll actually pay in today’s market. In the next section we’ll look at 2026 waterfront pricing trends by lake, river, and Long Island Sound so you know exactly what your budget can buy.

2026 Waterfront Pricing Trends by Lake, River & Long Island Sound

Classic multi-million-dollar waterfront estate directly on Long Island Sound in Greenwich, Connecticut.

As of February 2026, waterfront homes Connecticut pricing varies dramatically depending on location, water depth, dock rights, and views. Here’s the current market breakdown I’m seeing every week as a Connecticut real estate broker:

Long Island Sound Shoreline (Greenwich to Mystic) Median sale price: $2.1M – $4.8M Prime direct-frontage homes with deep-water docks and southern exposure: $5M – $15M+ What $3M buys: 4–5 bedrooms, 100+ ft of frontage, private beach rights What $8M+ buys: Estate-level properties with pools, guest houses, and protected deep-water mooring

Iconic multi-million-dollar home on Candlewood Lake with private dock and gazebo.

Candlewood Lake (the largest lake in Connecticut) Median sale price: $925,000 – $2.4M Premium lots with western exposure and deep water: $2.8M – $4.5M What $1.2M buys: Updated 3–4 bedroom home with 80–100 ft frontage and dock What $3.5M+ buys: Newer custom homes with boathouses and panoramic views

Connecticut River (Essex, Old Saybrook, Mystic area) Median sale price: $850,000 – $2.9M Direct riverfront with tidal access and dock: $3.2M – $6M+ What $1.1M buys: Charming 3-bedroom with river views and small dock What $4M+ buys: Historic or new-build estates with deep-water access and mooring

Stunning waterfront compound on the Connecticut River in the Mystic area.

Quick 2026 Reality Check

- Homes with deeded dock rights and deep water are selling 18–28% faster than those without.

- Properties in VE or high AE flood zones are seeing 10–15% price discounts to offset insurance costs.

- Newer or recently renovated homes command a 22% premium over “needs work” waterfront properties.

These numbers change weekly, which is why I run fresh comps and construction cost estimates for every client before they make an offer.

Now you know what the market actually looks like in 2026. In the next section I’ll share real buyer case studies — wins, near-misses, and the expensive lessons that only experience can teach.

Real Case Studies: Recent Connecticut Waterfront Wins & Expensive Lessons

This type of high-end Long Island Sound waterfront estate in Greenwich is what many buyers dream about — but success depends on knowing the hidden costs.

Case Study 1 – The $3.8M Greenwich Win A couple from New York fell in love with a direct Sound-front home listed at $3.8M. The listing photos were stunning, but during my pre-offer walkthrough I noticed early erosion at the seawall and water staining in the lower level. We brought in a marine contractor and negotiated a $425,000 seller credit for repairs and elevation work. The buyers closed, spent another $180k on preventive upgrades, and now enjoy the home with peace of mind — and insurance costs $40k lower than they originally feared.

Modern new-construction waterfront home on Candlewood Lake — similar to the “bargain” property in Case Study 2.

Case Study 2 – The Candlewood Lake “Bargain” That Almost Wasn’t A retired couple found a 4-bedroom lakefront home listed at $1.45M — $300k below recent comps. It looked like a steal until my structural inspection revealed major foundation settling and a failing septic system too close to the water. We walked away from the first deal and found them a better property at $1.68M that needed no major work. They saved over $250k in future repairs and sleep better every night.

Classic Connecticut River waterfront home in the Old Saybrook area — similar to the insurance-focused case below.

Case Study 3 – The Riverfront Insurance Reality Check A family from Boston targeted a beautiful tidal river property in Essex. The price was right, but the flood zone and elevation made insurance quotes come in at $14,200 per year. We pivoted to a nearby home with better elevation and lower risk, dropping their annual flood insurance to $4,800. They closed happier and with far lower carrying costs.

These are not hypothetical stories — they’re real clients I’ve worked with in the past 18 months. The common thread? Every single one said the same thing at closing: “Thank God we had a broker who actually understands construction.”

The lessons are clear: beautiful views can hide expensive problems, and the right Connecticut real estate broker makes all the difference.

Now let’s put everything together. In the next section I’ll give you my exact step-by-step checklist so you can buy waterfront in Connecticut confidently in 2026.

Step-by-Step: How to Buy Waterfront Homes Connecticut Safely in 2026

A professional inspector examining the foundation and lower level of a waterfront home — this step saves buyers thousands.

Buying waterfront homes Connecticut in 2026 doesn’t have to be stressful if you follow the right process. Here is the exact 10-step checklist I give every client:

- Start with the right broker Work with a Connecticut real estate broker who has real construction experience (not just someone who shows listings). I personally review every property with a builder’s eye.

- Get an immediate flood determination report Order this the same day you like a house — it tells you the exact zone and required elevation.

- Hire a licensed land surveyor Confirm property lines, mean high water line, and any encroachments before you make an offer.

A surveyor measuring a waterfront lot — essential for understanding exactly what you’re buying.

- Bring in a marine contractor or coastal engineer They inspect docks, seawalls, bulkheads, and erosion risk.

- Order a full elevation certificate This document determines your actual flood insurance cost.

- Test septic system and well (if applicable) Waterfront properties often have aging systems that fail when water tables rise.

- Get multiple flood insurance quotes early Compare NFIP vs private carriers before you’re under contract.

- Review all shoreline permits and history Check with the town and CT DEEP for any open violations or required repairs.

- Negotiate with full knowledge Use the inspection findings to ask for credits, repairs, or price reductions — I handle this for every client.

- Close with the right team A real estate attorney experienced in waterfront transactions plus your broker who understands construction.

Follow these steps and you’ll avoid 95% of the expensive surprises I see other buyers face.

As your customer-first Connecticut real estate broker, I guide you through every single one of these steps — no pressure, just clear answers and construction insight you won’t get anywhere else.

Ready to start? The next (and final) section wraps everything up with my best advice and how to reach me directly.

Conclusion & Next Steps

Waterfront living in Connecticut in 2026 offers incredible rewards — private docks, breathtaking views, strong appreciation, and a lifestyle most people only dream about.

But as we’ve covered in this guide, those rewards only last when you go in with eyes wide open about flood zones, insurance costs, shoreline regulations, and hidden structural issues.

The good news? You don’t have to figure it all out alone.

Golden hour on the Connecticut waterfront — the peaceful lifestyle that makes it all worthwhile.

If you’re serious about buying waterfront homes Connecticut (or land to build your dream home with BIOS Homes), the smartest next step is a quick, no-pressure conversation.

I’ll personally review any property you’re considering, run the real numbers on flood insurance and construction costs, and give you straight answers based on 45 years of experience — no sales pitch, just honest guidance.

Text or call me directly at 203-994-3950 Or book a free 30-minute Property Strategy Call here: [Calendly link]

Whether you’re just starting your search or ready to make an offer, I’m here to help you buy with confidence and avoid the expensive surprises that catch other buyers off guard.

You deserve a waterfront home you’ll love for decades — not one that becomes a financial burden.

Let’s make that happen together.

Steve Schappert Customer-First Connecticut Real Estate Broker 45 Years Experience • Construction Insight You Won’t Find Anywhere Else Connecticut Real Estate Brokerage LLC Text “waterfront” to 203-994-3950 for fastest response